See also

28.01.2026 11:47 AM

28.01.2026 11:47 AMA week earlier, we suggested that the pound had good chances to resume growth, but that stronger movement would require additional catalysts. These catalysts have now appeared, and from several directions at once, which allows us to expect further development of the bullish trend.

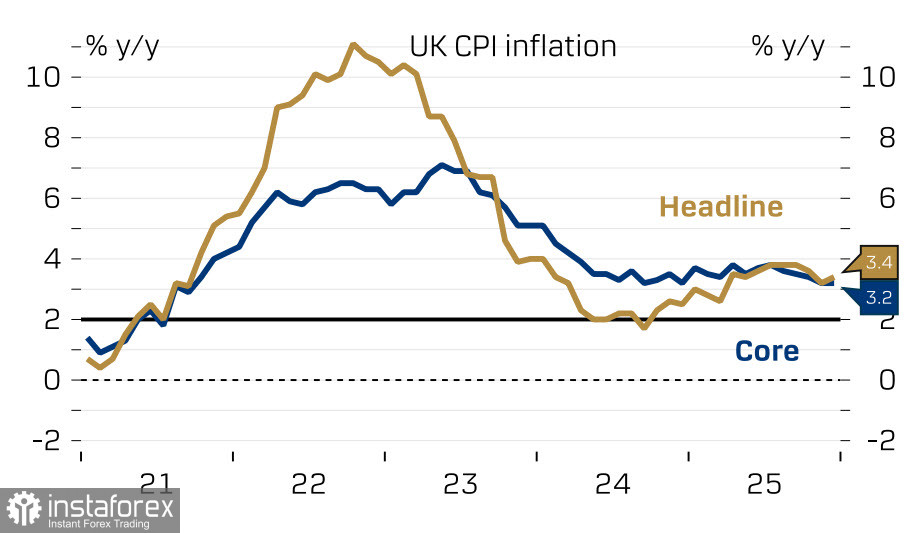

Let us start with economic news. The Consumer Price Index in December rose to 3.4% year-on-year, exceeding forecasts, and even though core inflation remained unchanged at 3.2%, it can be said with confidence that there are still no signs of a slowdown in price growth at this point.

Other indicators are also entirely in the green zone: retail sales growth in December amounted to 2.5% year-on-year versus a forecast of 1%; the retail price index rose more strongly than expected, supporting inflation; business activity in January increased noticeably in both key sectors—manufacturing rose from 50.6 to 52.6, while services showed an even stronger increase from 51.4 to 53.9. The composite index is at its highest level since spring 2024. PMI growth suggests that the positive economic momentum observed in November and December will continue into January.

The main conclusion is that inflationary pressure is at least not easing amid an economic recovery. These two factors alone, even without considering the labor market, are sufficient to confidently forecast the outcome of the Bank of England meeting on February 5—the interest rate will remain unchanged at 3.75%.

At the December meeting, the Bank of England cut the rate by a very narrow vote (5 to 4). Given the new data, conditions for further easing have not only failed to materialize, but have instead noticeably diminished. This is a bullish factor for the pound even without considering all other influences.

There is, of course, also the external political backdrop. On Tuesday, US President Trump accelerated the weakening of the dollar by stating that he is not concerned about its decline. "The dollar feels great," Trump commented. Markets interpreted these words as a signal to continue selling the dollar, since a weaker dollar stimulates exports. Given that there are no signs of increased activity in the US industrial sector despite strong support from the administration, at least through import restrictions, a weaker dollar in the current environment appears justified as a means of further stimulating domestic production.

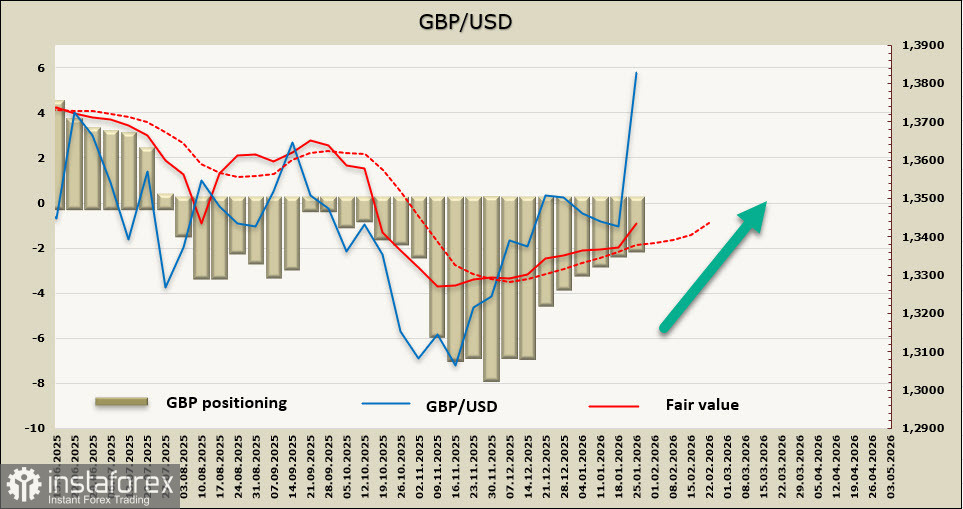

The net short position on the pound changed only slightly over the reporting week, while the calculated price remained above the long-term average and accelerated its growth.

A week earlier, we identified a target at 1.3566, which was quickly reached. Just as rapidly, the pound moved through the next resistance at 1.3725, then updated the high at 1.3787 and consolidated above it. The pound is already trading at September 2021 levels. The next target is 1.4240, and it is still unclear whether it will be reached in the near term. Considering that gold is already around 5,300 and Brent crude is at its highest level since September last year, we assume that the momentum toward dollar weakening remains strong. The FOMC meeting will take place today, and surprises are almost guaranteed—if not on the rate decision, which will most likely remain unchanged, then at least during Jerome Powell's press conference, as too many unresolved issues remain on the agenda.