یہ بھی دیکھیں

18.03.2026 12:47 AM

18.03.2026 12:47 AM

*see also: Trading indicators for SILVER (XAG/USD)

The US dollar index, USDX, has corrected downward from the psychological level of 100.00.

However, gold has not been able to capitalize on this classic opportunity for growth, remaining virtually unchanged, as we noted in our review, "XAU/USD: The Dollar Falls, but Gold Does Not Rise. What Is Happening in the Market?"

Silver shows a similar picture. Instead of rising, its price is moving in a narrow range with a downward inclination.

Despite the weakening of the US dollar and the escalation of the Middle Eastern conflict, silver remains under pressure, consolidating around 79.00-82.00 dollars per ounce after a recent drop to a two-week low near 77.00.

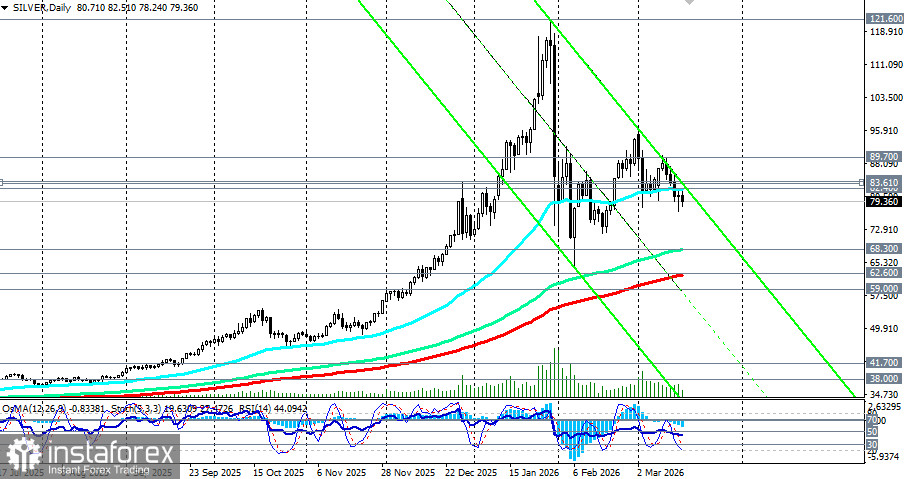

Silver experienced strong growth in 2025-2026, reaching multi-year highs amid high demand from both industry and investors. However, in recent weeks, a correction has been observed: the metal is testing lower levels than one might expect given the weak dollar.

During the correction, silver moved in a volatile manner, sometimes significantly — for example, declines were driven by a strengthening dollar and rising expectations for Fed rate hikes.

High real rates and US Treasury yields diminished the appeal of non-yielding assets like silver. Even in moments when the dollar is weak, the silver market has already closed part of its long positions, and the metal needs strong trend confirmation to secure itself above resistance, economists say.

The January jump in silver above 120.00 was extraordinary — the metal posted its strongest gain since 1979. However, a harsh correction followed, bringing it to 70.00–80.00. Such movement in January knocked many investors out of the market who entered long positions on pullbacks and drops to those levels, and the current consolidation additionally reflects the exhaustion of buying momentum.

At the same time, unlike gold, which is the primary safe haven, silver has a significant industrial component of demand — it is used in electronics, solar panels, medicine, and other sectors.

This means that silver's movement depends not only on risk sentiment and the dollar's position but also on the state of global industrial demand. If the industry holds back purchases and investment funds exit positions, then the price may not react to fundamentally positive signals regarding the dollar/geopolitics in the same way that gold does.

Silver is in a unique situation: the market is anticipating a sixth consecutive year of structural deficit — 67 million ounces in 2026. Physical demand will again exceed supply, which should support prices. However, investment demand and industrial consumption show divergent dynamics.

Solar energy remains a key driver of demand — consumption is forecasted to reach 160 million ounces in 2026. However, manufacturers are actively implementing technologies to reduce the silver content in each panel and replacing it with alternative materials, which has already led to a decline in demand from the PV sector.

Meanwhile, the market is paused in anticipation of key events this week — meetings of major central banks that will define the future trajectory of monetary policy amid the oil shock and geopolitical uncertainty.

Upcoming policy decisions from the Fed, ECB, Bank of England, Bank of Japan, Bank of Canada, and Swiss National Bank come at a particularly sensitive time. Although all are expected to maintain rates at current levels, the key will be the statements of intent and assessment of the oil shock's impact on inflation.

Economists note that concerns about the Fed's independence and uncertainty in US policy continue to support investments in precious metals. However, any hint of premature easing could amplify inflation expectations, while maintaining a hawkish rhetoric could strengthen the dollar.

The Bank of England is also expected to keep the rate at 3.75%, pushing expectations for easing further out. The Bank of Japan remains the only central bank maintaining an ultra-loose policy, supporting the yen as a safe-haven currency, but not directly affecting silver.

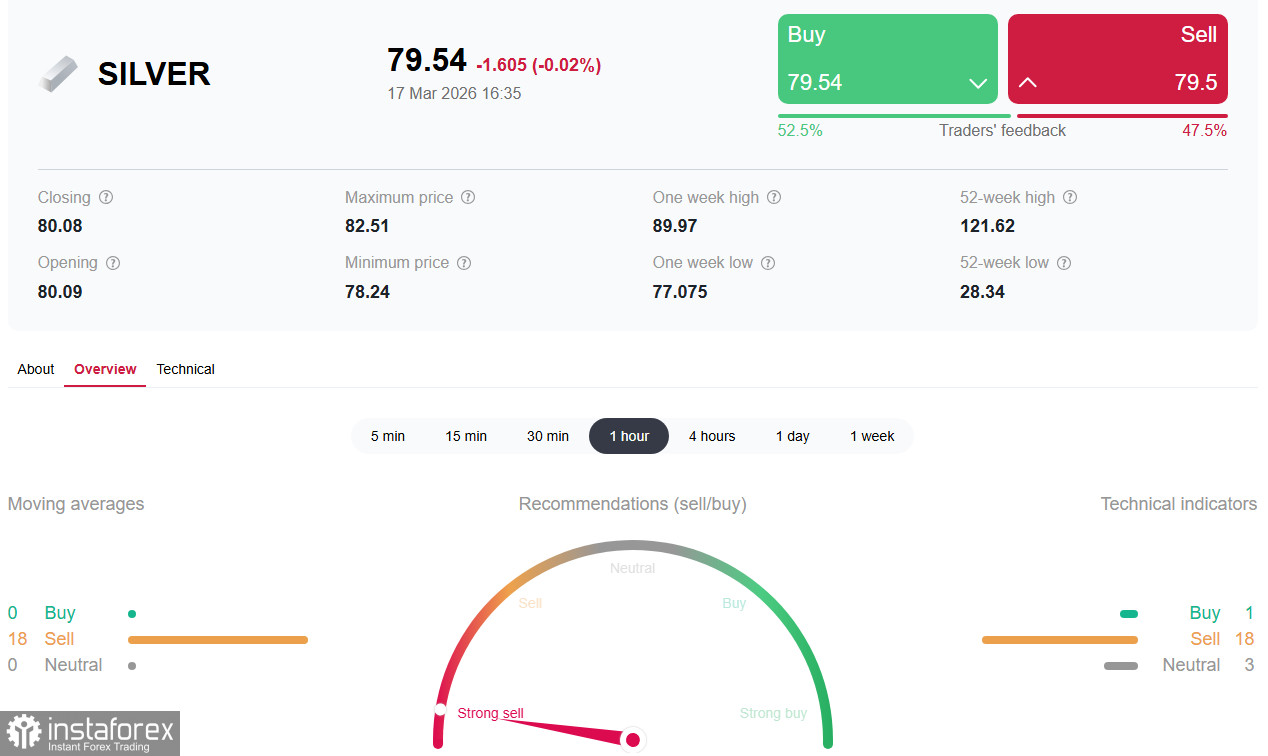

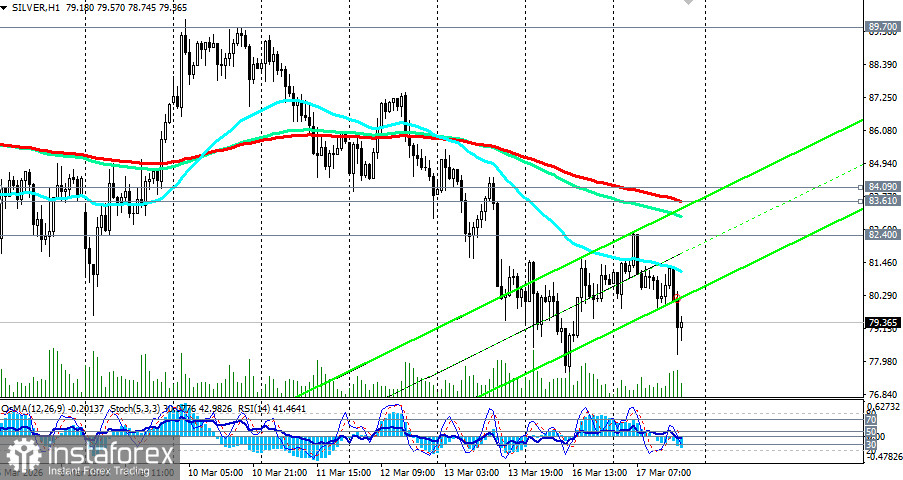

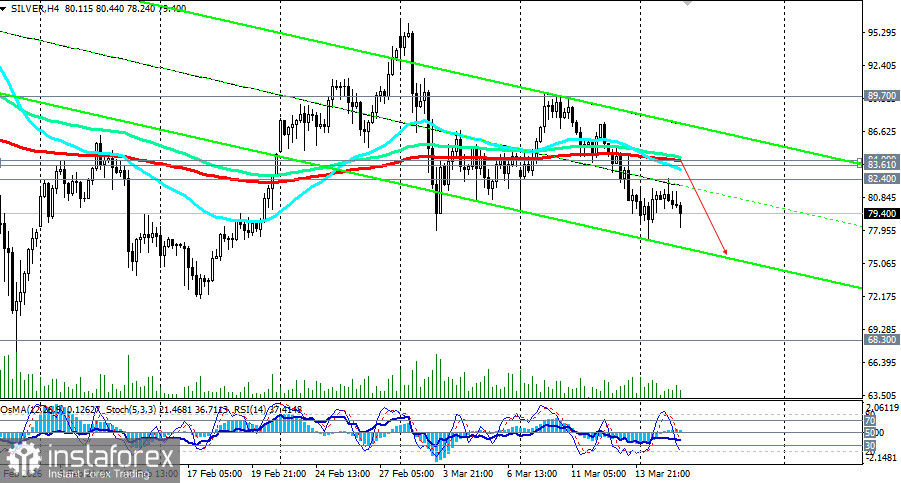

Resistance: 83.61, 84.09, 84.50 (short-term), 87.00–92.00 (key zone), 96.40 (March highs)

Support: 79.00–82.00 (psychological zone), 70.00–72.00 (main support of 2026), 68.30-62.60 (key support and EMA144, EMA200 on the daily chart)

Until the FOMC announcement on Wednesday, silver is likely to remain within the consolidation range of 78.00–85.00. Technical indicators suggest the possibility of a rebound to 84.00–86.00, but for a confident reversal, a solid hold above 84.50 is required.

Scenario A (bearish): a breakdown below 78.00 will open the way to 76.00–77.50 and further to 72.00–70.00.

Scenario B (bullish): holding above 80.00-82.00 and a breakout at 84.50 will allow testing 87.00–92.00, and then 96.40.

Medium-term forecast (2026)

Economists forecast an average price of 81.00 per ounce in 2026, with peaks in the 2nd quarter at 84.00 and in the 4th quarter at 85.00. They emphasize that volatility will remain high and that the market will be sensitive to any signals on interest rates. Sustained deficits and support from gold should limit downside risks. However, technical factors and investor positioning will play a key role.

The silver market is experiencing a unique moment in which classic support factors — a weakening dollar and geopolitical tension — are offset by a radical reassessment of expectations for monetary policy and by technical overbought conditions after the January rally.

The key zone of 80.00–84.00 will become decisive in the coming days. The Fed meeting on Wednesday will determine whether silver can hold support or continue its correction to 70.00–72.00. Any hints at maintaining a tight policy will send the metal to the lower boundary of the range, while cautiously "dovish" signals may provoke a rebound to 90.00–92.00.

In any scenario, volatility will remain high. Investors should closely monitor developments in diplomatic contacts around the Strait of Hormuz, inflation data, and, most importantly, the rhetoric of central banks on how they interpret the combination of slowing economic growth and inflationary risks from the oil shock. The sixth year of structural deficit creates long-term support, but the path to new highs will be arduous and dependent on the monetary policy of the world's major central banks.